Predicting financial market stress remains a daunting challenge. Traditional models often fall short in capturing the intricate and nonlinear dynamics that drive market instability. However, recent advancements in AI technology are starting to offer fresh solutions. This article explores two significant breakthroughs in AI that are helping to identify financial stress signals before they escalate.

AI Tools That Can Detect Market Stress Before It Hits

As financial systems become more interconnected, the task of spotting potential crises early has never been more critical. Past global disruptions, like the 2008-09 financial meltdown, underscore the importance of finding ways to predict stress in real-time. Traditional econometric models often miss the mark, failing to account for the complexity of modern markets and their interconnections.

AI’s ability to analyze vast datasets has opened up new pathways for predicting financial stress. While AI has long been used in asset pricing (Kelly et al., 2024), it’s now finding a place in financial stability monitoring (Fouliard et al., 2021). Yet, AI’s “black-box” nature has hindered its ability to provide clear, actionable insights for policymakers.

This article showcases recent research (Aldasoro et al., 2025; Aquilina et al., 2025) that addresses the limitations of AI by enhancing its transparency and providing useful insights for financial decision-makers. These studies highlight AI’s potential to predict market stress and the underlying drivers of market dysfunction.

Understanding Financial Market Stress: A Complex Puzzle

Market stress is a broad concept that can manifest in different ways, such as liquidity crises, price instability, or disruptions in market efficiency. Major events like the LTCM collapse in 1998 or the 2008-09 financial crisis show how stress can start in isolated markets before spreading across the entire system. As financial systems evolve, we are seeing an increasing shift in stress from traditional banks to non-bank financial institutions.

Traditional models designed to detect financial crises often fall short, especially when predicting non-linear interactions or feedback loops that amplify stress. These models tend to have high false positive rates, which makes it difficult to identify real threats in time.

Machine learning (ML) offers an exciting alternative. Unlike traditional models, ML algorithms can analyze vast, complex datasets and detect hidden relationships. The studies examined in this article illustrate how these tools can not only predict market stress but also help policymakers take timely action.

Using Machine Learning to Predict Market Stress

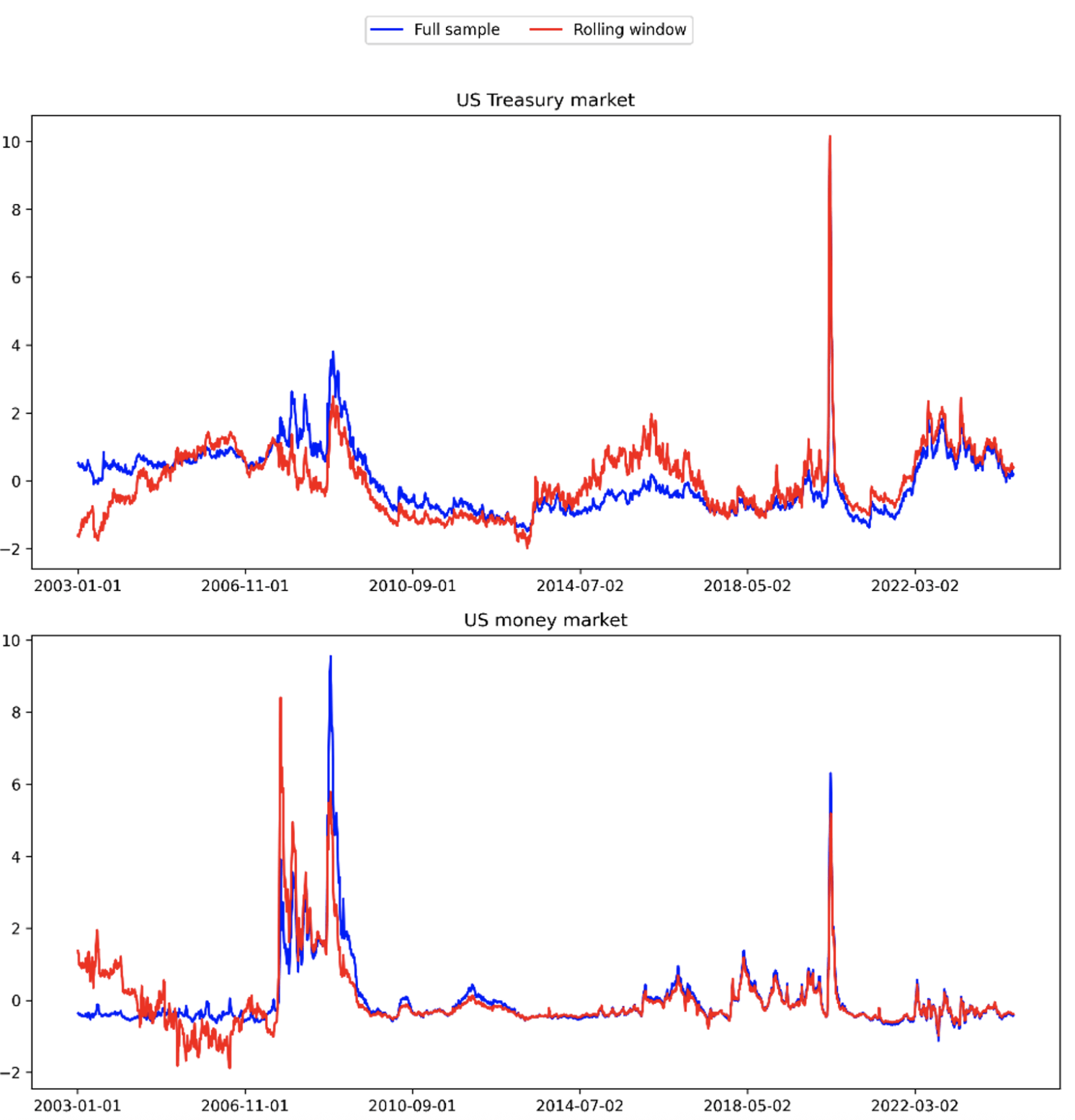

Aldasoro et al. (2025) introduce a novel machine learning framework that predicts financial market stress. Their method begins by developing Market Condition Indicators (MCIs) for three key US markets: Treasury, foreign exchange, and money markets. These indicators capture crucial signals such as liquidity shortages, volatility spikes, and arbitrage breakdowns.

Figure 1: Market condition indices for US Treasury, foreign exchange, and money markets

Notes: This figure displays the five-day moving average of market condition indices for the US Treasury, money, and foreign exchange (FX) markets, shown in the upper, middle, and lower panels, respectively. The data covers the period from 01/01/2003 to 31/05/2024.

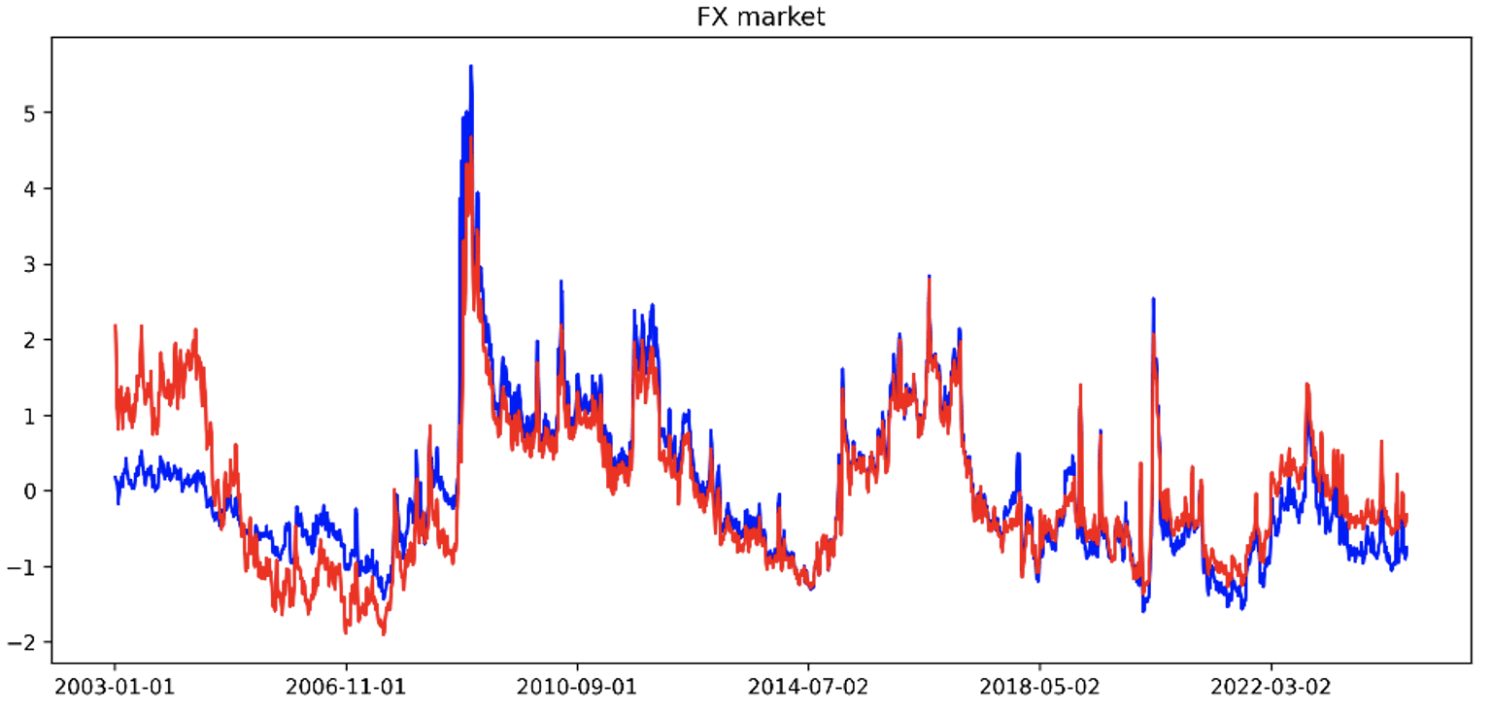

To forecast market conditions, the team uses random forest models, a machine learning algorithm that leverages multiple decision trees. By averaging the predictions of these trees, random forest models are able to reduce the risk of overfitting. The results are striking: these models outperform traditional time-series approaches, especially when predicting tail risks over longer periods.

One of the key innovations in this research is the use of Shapley value analysis, which explains the primary factors influencing market stress predictions. The analysis reveals that macroeconomic uncertainty, particularly around monetary policy, plays a major role in driving market instability. Additionally, liquidity conditions and the state of the global financial cycle are key contributors. These insights make the model not only more accurate but also more interpretable for policymakers.

Figure 2: Forecast accuracy of random forest and autoregressive models

Notes: This figure compares the quantile losses of the random forest and autoregressive models using out-of-sample predictions across various forecast horizons. Negative values suggest superior performance by the random forest model.

Blending Numerical Data and Textual Insights with AI

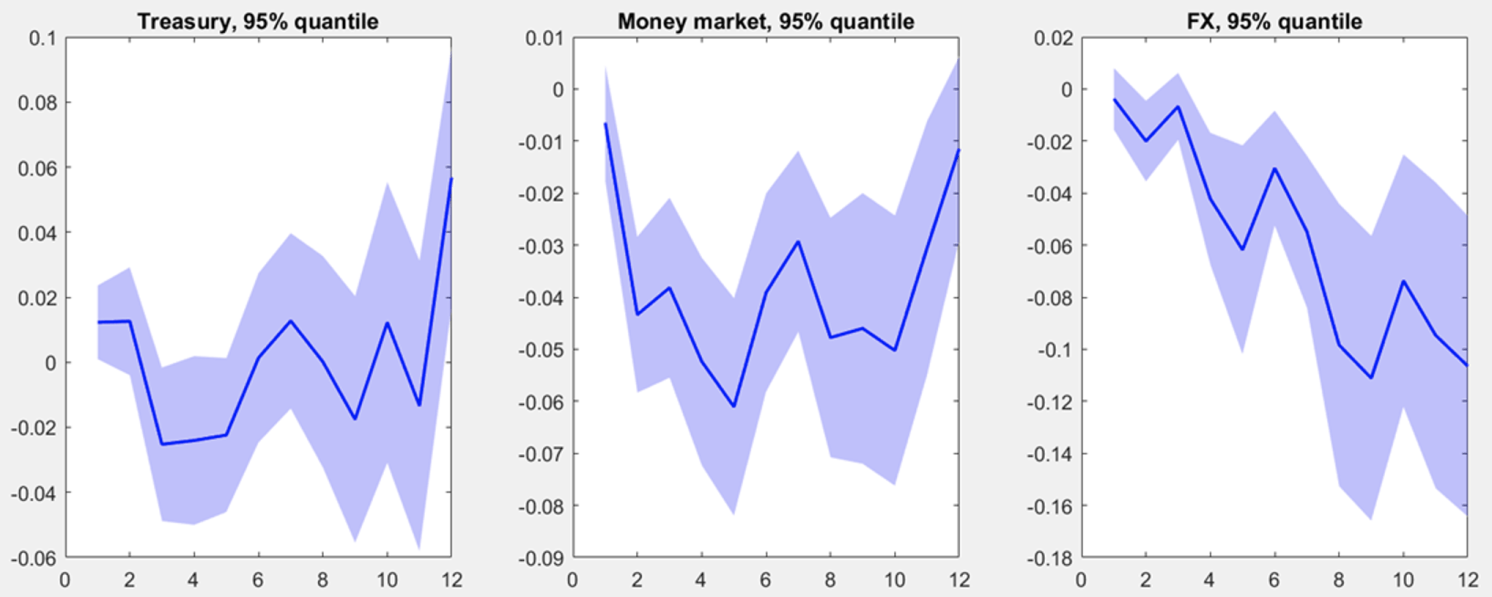

Aquilina et al. (2025) take a different route by combining numerical data with textual information from financial news. Their research focuses on predicting disruptions in the foreign exchange market, specifically by monitoring deviations in triangular arbitrage parity (TAP) in the euro-yen pair. They integrate recurrent neural networks (RNNs) with large language models (LLMs) to create a two-stage forecasting system.

The RNN detects deviations in TAP up to 60 working days in advance, providing a one-month warning of potential market stress. Through out-of-sample testing, the model demonstrated its practical value. For instance, it flagged increased risks ahead of the March 2023 banking crisis, even though it was trained on data available only through 2020.

Figure 3: Predictive accuracy of market dysfunction episodes

Notes: True data represents the 20-day average of the daily euro-yen triangular arbitrage parity difference, using the US dollar as the vehicle currency, calculated on a minute-by-minute basis. The vertical red dashed line marks the end of the training period (end-2020); data to the right of this line is treated as pseudo out-of-sample.

To tackle the “black-box” issue, Aquilina et al. (2025) developed a new framework that assigns dynamic weights to various indicators. These weights are then used by the LLM to scan financial news for contextual insights. In the March 2023 banking turmoil, for example, the model identified risks related to euro liquidity and cross-currency arbitrage, and the LLM flagged articles about tightening dollar funding and rising geopolitical tensions. This combination of statistical analysis and narrative context makes the predictions more actionable for policymakers.

Policy Implications: AI’s Role in Financial Stability

While more research is needed, these advancements highlight the growing potential of AI to monitor and predict financial market stress. The studies show that machine learning models can be an effective tool for forecasting market conditions, especially in the face of complex, interconnected systems.

By integrating numerical data with qualitative insights from financial news, policymakers can now get a fuller picture of market dynamics. Combining these quantitative forecasts with textual analysis offers a more complete understanding of potential risks.

The ability to interpret AI models is crucial for their successful adoption in policymaking. Techniques like Shapley value analysis and dynamic weighting provide transparency, helping policymakers understand what drives market stress. This makes AI tools not only more accurate but also more reliable for decision-making.

The Path Forward for AI in Financial Market Monitoring

AI’s role in detecting financial market vulnerabilities is just beginning. With innovations like machine learning and large language models, policymakers can gain better foresight into market stress, allowing them to act quickly to mitigate risks. However, challenges remain, including the need for robust computational resources and the risk of overfitting in some models.

To fully harness the power of these AI tools, financial regulators must invest in the infrastructure necessary to process large-scale data. As these technologies continue to evolve, they promise to transform how we monitor and manage financial stability in the future.

References

- Aldasoro, I, P Hördahl and S Zhu (2022), “Under pressure: market conditions and stress”, BIS Quarterly Review (19): 31–45.

- Aldasoro, I, P Hördahl, A Schrimpf and X S Zhu (2025), “Predicting Financial Market Stress with Machine Learning”, BIS Working Papers No. 1250.

- Aquilina, M, D Araujo, G Gelos, T Park and F Pérez-Cruz (2025), “Harnessing Artificial Intelligence for Monitoring Financial Markets”, BIS Working Papers No. 1291.

- Du Plessis, E and U Fritsche (2025), “New forecasting methods for an old problem: Predicting 147 years of systemic financial crises”, Journal of Forecasting 44 (1): 3-40.

- Fouliard, J, M Howell, H Rey and V Stavrakeva (2021), “Answering the queen: Machine learning and financial crises”, NBER Working Paper 28302.

- Huang, W, A Ranaldo, A Schrimpf and F Somogyi (2025), “Constrained liquidity provision in currency markets”, Journal of Financial Economics 167: 104028.

- Kelly, B, S Malamud and K Zhou (2024), “The Virtue of Complexity in Return Prediction”, Journal of Finance 79: 459-503.

- Pasquariello, P (2014), “Financial Market Dislocations”, Review of Financial Studies 27(6): 1868–1914.